Bitcoin Mining Progress Reaches 89% — Do Miners Still Have Influence?

Previously, CryptoQuant tweeted that the amount of Bitcoin flowing from miners to exchanges is at its lowest point in a year, having declined from its peak in May. This suggests miners are Bitcoin.

We all know that since the first Bitcoin was mined on January 3, 2009, Bitcoin has undergone three halving events, with block rewards declining from the initial 50 coins to the current 6.25 coins. At Bitcoin's average block time of 10 minutes, the current daily global miner output is approximately 900 Bitcoin.

OKX market data shows that spot BTC/USDT has a 24-hour trading volume of 22,600 coins. Even if miners were to sell their entire daily output through "mine and dump," the impact on the market would be negligible.

Currently, Bitcoin's circulating supply stands at 18.7297 million coins. Compared to the 21 million cap, Bitcoin's mining progress has reached 89%, with only 2.2703 million coins remaining unmined. If Bitcoin halves again in four years, daily production will drop to just 450 coins, making daily miner selling pressure even more negligible. As miners transition from producers to network service providers, do they still hold significant influence? Which miner indicators can we reference? And what happens once Bitcoin is fully mined? Let's explore these questions today.

Miners Are Natural Sellers, But the Volume Flowing to Exchanges Is Small

Bitcoin has no centralized issuing body — all issuance is generated through mining competition by network miners. Since miners primarily acquire Bitcoin through mining rather than purchasing, and the costs of mining (mining equipment, electricity, rent, etc.) are denominated in fiat currency while their revenue is in Bitcoin, miners are natural net sellers.

In the past, whenever coin prices dropped, people would immediately think of miner selling. This was because Bitcoin's market cap was smaller at the time, miners held more tokens, and new Bitcoin was continuously being produced daily. Their selling signals often came with group behavior, making their impact on the market substantial. However, as this bull market took off and institutional players led by Grayscale began aggressive buying, the market shifted its focus to institutions.

Take Grayscale as an example. According to The Block data, Grayscale held 448,400 Bitcoin on October 1 of last year, and by February 1 of this year, its holdings reached 648,000 Bitcoin — an increase of 199,600 Bitcoin over four months, or approximately 1,621 Bitcoin added daily. During the same period, based on Bitcoin's average block time of 10 minutes and a block reward of 6.25 coins, daily production was 900 Bitcoin — Grayscale's daily demand was 1.8 times miner output. And Grayscale was clearly not the only buyer at the time. Companies like MicroStrategy, Square, and Tesla placed buy orders worth tens of millions of dollars, exacerbating the supply-demand imbalance. The direct result was that Bitcoin surged from an opening price of $10,777.7 on October 1 to a closing price of $57,142.1 by the end of April — a gain of 430%.

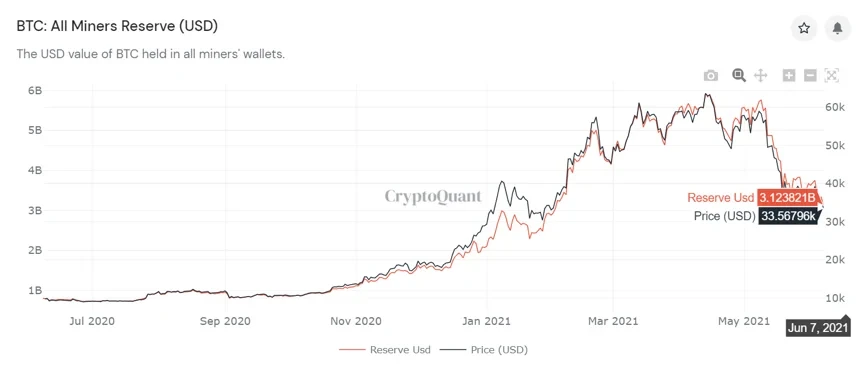

CryptoQuant data shows that Bitcoin miners currently hold reserves worth approximately $3.124 billion. In comparison, OK Link records institutional Bitcoin holdings at $16.816 billion, accounting for 2.75% of Bitcoin's total market cap. Clearly, institutional holdings already exceed miners' on-chain Bitcoin deposits.

Coin Metrics published an article in late February titled "FOLLOWING FLOWS II: WHERE DO MINERS SELL?" — primarily aimed at assessing the scale and impact of miner selling. The article concluded that given the small ratio of miner deposits to total exchange inflows and the lack of correlation between miner exchange inflows and price, it can be essentially confirmed that miners are not the cause of Bitcoin's decline.

This is also evident from recent on-chain data. Combining Glassnode and CryptoQuant data, miners produced a total of 6,300 Bitcoin over the past seven days, while only 1,724.98 Bitcoin flowed to exchanges. Compared to the total Bitcoin exchange inflow of 205,200 coins over the same period, miners' Bitcoin flowing to exchanges accounts for less than 1%.

Mining Progress at 89% Complete — Market Price Influenced by Short-Term Speculators

CoinMarketCap data shows that 89% of Bitcoin has already been mined, with only 2 million or so Bitcoin remaining to be mined. As halving occurs every four years, Bitcoin's daily production will only continue to decrease. Since we already know the volume of Bitcoin flowing from miners to exchanges is small, the declining influence of miners is an undeniable fact.

We all know that Bitcoin's initial bull run was driven by strong buying pressure. But now that Bitcoin has entered a nearly two-month downward trend, it can only mean that supply far exceeded demand during this period. As natural sellers, miners are naturally on the supply side. However, even as miners are holding back from selling, Bitcoin's price continues to decline and exchange balances are rising — who is doing the selling?

Several years ago, when Jiang Zhuo'er explained Bitcoin to the public, he discussed Bitcoin's supply and demand dynamics. He categorized Bitcoin demand into three types: (1) purchasing Bitcoin for store of value and investment, to hedge against inflation; (2) purchasing Bitcoin for use cases such as payments, cross-border remittances, and settlements; and (3) purchasing Bitcoin for speculation and trading. Bitcoin supply, on the other hand, falls into two categories: (1) miners selling their mining proceeds; and (2) holders who purchased Bitcoin for store of value, investment, or speculation selling their holdings. Category (3) on the demand side and category (2) on the supply side are the primary drivers of Bitcoin's price volatility.

Yesterday, in our article "Market Continues to Weaken — Who Is Selling Bitcoin?", we mentioned that Tesla sold 10% of its Bitcoin holdings in Q1 2021, generating $272 million in revenue and $101 million in profit. UK asset management firm Ruffer disclosed that it invested $600 million to purchase Bitcoin in November 2020 and sold its final Bitcoin position in April, ultimately realizing total profits exceeding $1.1 billion.

Glassnode's Week 22 weekly report noted that throughout May, a total of 155,000 Bitcoin transitioned from holding to liquid or highly liquid states, with short-term holders increasing their selling volume by more than 5x during this sell-off — consistent with Jiang Zhuo'er's supply category (2). In other words, this decline was caused by users who purchased Bitcoin for investment or speculative purposes (such as institutions that entered during the early bull run or retail investors who followed institutional进场) choosing to take profits when their gains were substantial, or exiting when they perceived greater risk than opportunity ahead.

As more Bitcoin is mined and secondary market circulation far exceeds what miners hold, miner influence is weakening. But why should we still monitor miner indicators?

First, Bitcoin mining requires substantial human and material resources and cannot be easily shut down in the short term. Once mining begins, it runs on a multi-year basis. Therefore, miners are viewed as Bitcoin's most dedicated supporters, or at least as a group that believes in Bitcoin's future prospects. When miners begin aggressively selling Bitcoin, it often signals pessimism about Bitcoin's future. As an indicator akin to market faith, wavering miner sentiment can also influence retail investors' decisions.

Second, miner indicators can serve as a tool for identifying bull market tops and bear market bottoms. For example, in our article "Market Forces Balance, Price Action Arrives at a Crossroads", we introduced the Puell Multiple — an indicator developed to track miner activity. The Puell Multiple is calculated by dividing Bitcoin's daily issuance price (in USD) by the 365-day moving average of the daily issuance price, measuring miners' profitability.

A high Puell Multiple indicates high profitability — at such times, miners accumulate Bitcoin at a cost far below market price and have an incentive to sell for greater profits. A low Puell Multiple indicates low profitability — in this situation, miners face revenue pressure. If pressure persists, they may be forced to shut down mining equipment, eventually leading to exit and forming a bear market bottom. Of course, miner indicators can also serve as a reference for market supply-demand transitions, helping to identify where selling pressure is coming from.

Lastly, unusual activity from early miner addresses still commands attention in the community. The famous "疑似中本聪地址抛售Bitcoin" event that once occurred in the space caused Bitcoin to crash in the short term. If an address dormant for over a decade suddenly becomes active, empties its wallet, and transfers to an exchange, it will inevitably attract market attention. Even today, there remains a group of people dedicated to studying Satoshi's mining behavior — this too is part of what constitutes the faith indicator.

Bitcoin Miner Revenue Falls Short of Ethereum — What Happens After Mining Is Complete?

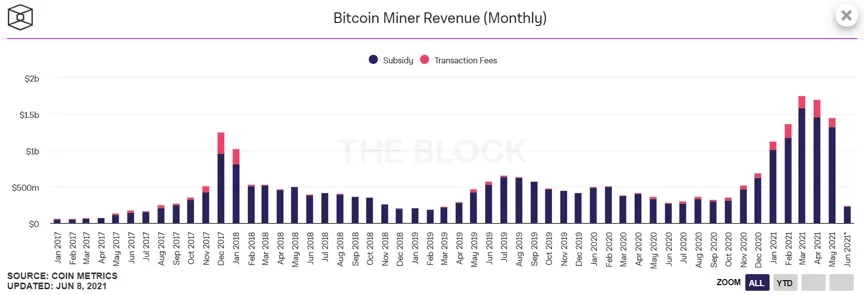

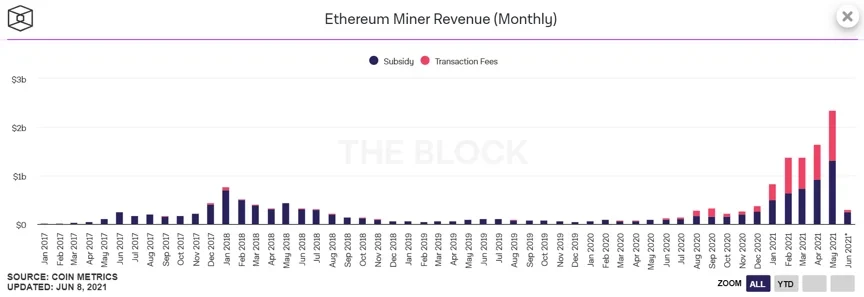

Recently, The Block published on-chain data for May, showing that Ethereum surpassed Bitcoin across multiple metrics — one being that "Bitcoin miner revenue fell 15% to $1.45 billion, while Ethereum miners posted record-high revenue of $2.35 billion in May."

We all know that current Bitcoin and Ethereum miner revenue consists of two components: block rewards and transaction fee income. In the charts below, transaction fee revenue is shown in red and block rewards in blue. Ethereum's red segment has been growing notably, with transaction fees on Ethereum reaching $1.03 billion in May, accounting for 43.8% of total revenue — Ethereum's transaction fee income and block rewards appear increasingly balanced. For Bitcoin, miner revenue is still dominated by block rewards. Using May as an example, transaction fees totaled less than $124 million, accounting for only 8.6% of total revenue.

We all know that the significant increase in transaction fees on Ethereum is closely tied to the growth of the DeFi ecosystem and surging on-chain activity — which also aligns with Ethereum's transition roadmap. But turning to Bitcoin, we can't help but wonder: since everyone knows there will come a day when Bitcoin is fully mined, once all Bitcoin has been issued, miner revenue will come entirely from transaction fees. Since miners are the primary force maintaining Bitcoin's network security, their incentive to participate in the Bitcoin network is driven by revenue. Unless Bitcoin prices continue to rise substantially, on-chain revenue alone will struggle to provide sustained motivation. Additionally, Bitcoin has limited on-chain applications — Omni-layer USDT activity is far less than ERC20 and TRC20 USDT activity. A large amount of Bitcoin has also been wrapped and bridged to the Ethereum network to participate in DeFi activities, further reducing Bitcoin's on-chain activity. Glassnode data shows that Bitcoin's on-chain active address count has fallen to its lowest level in nearly a year, and declining network activity will also reduce transaction fee revenue.

So, what happens after Bitcoin is fully mined? According to the original vision, even once all Bitcoin has been issued, as long as there is sufficient trading demand, miners will have reason to continue mining. Moreover, due to Bitcoin's deflationary mechanism, Bitcoin's price will continue to rise, and transaction fee revenue will naturally increase accordingly.

However, during this bull market, we can clearly observe that Bitcoin's on-chain trading volume has not increased significantly compared to the previous bull market, whereas Ethereum's trading volume has seen a notable surge.

Additionally, Bitcoin's transaction fees are affected by byte size and network congestion. Currently, Bitcoin transfers charge 0.0001 BTC per kilobyte. If too many people are transacting on-chain and the network becomes congested, users will pay higher fees to prioritize their transactions for inclusion in blocks. If Bitcoin's price continues to rise — say to $100,000 — fees per kilobyte would reach $10.

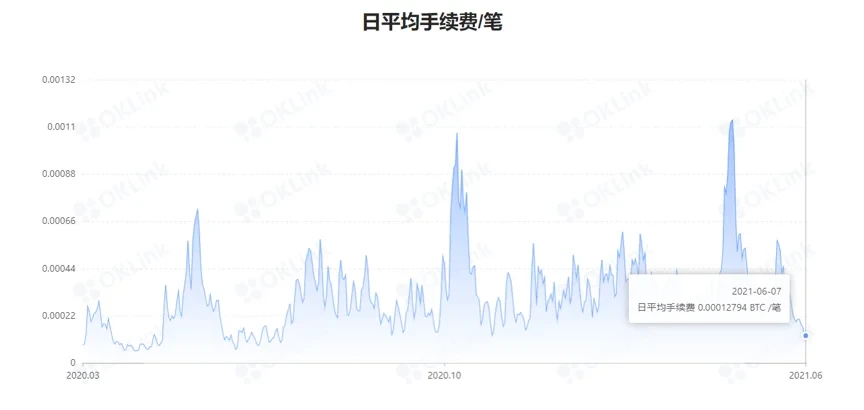

OK Link data shows that Bitcoin's average daily transaction fee on June 7 was 0.000128 BTC per transaction, approximately $4.25.

Clearly, Bitcoin has evolved from Satoshi Nakamoto's envisioned medium of value exchange into a store of value. If Bitcoin continues to appreciate, on-chain fees will naturally increase as a result. But how high would fees need to rise before on-chain transaction fee revenue becomes the primary source of miner income and continues to incentivize miners to produce new blocks after Bitcoin is fully mined? We cannot provide a specific figure at this time. Moreover, rising Bitcoin prices could also reduce or draw criticism for on-chain activity due to high fees. Additionally, because of Bitcoin's low TPS, some high-frequency applications have already migrated elsewhere — such as Omni-USDT. Ethereum DeFi has also locked a portion of Bitcoin permanently on-chain, while HODLers prefer to accumulate Bitcoin rather than use it. One can only imagine what on-chain activity looks like. Sufficient trading demand, sustained price appreciation, and the development of alternative chains — the relationship between these three factors may become a significant constraint on Bitcoin network development in the future.

Disclaimer

This article may contain product information not applicable to your region. This article is intended to provide general information only and makes no representation as to any factual errors or omissions. This article represents the author's personal views only and does not constitute the views of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holdings in digital assets (including stablecoins) involve a high degree of risk and may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets is appropriate for you based on your financial situation. For questions about your specific circumstances, please consult your legal/tax/investment professional. The information contained in this article (including market data and statistical information, where applicable) is provided for general reference purposes only. While all reasonable precautions have been taken in the preparation of such data and charts, we accept no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, and excerpts of 100 words or less may be used, provided that such use is for non-commercial purposes only. Any reproduction or distribution of the full article must prominently state: "This article is copyrighted © 2025 OKX, used with permission." Permitted excerpts must cite the article title and include attribution, for example: "Article title, [author name (if applicable)], © 2025 OKX." Some content may have been generated or assisted by artificial intelligence (AI) tools. Derivative works and other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Ushering in a New Era of Next-Gen Crypto Payments

The choice of tens of millions of users. Register with OKX to enjoy an exceptional trading experience and diverse wealth management products. A letter from OKX CEO Star: Today, we are officially launching the first version of OKX Pay to over 100 million global users. As the industry's first truly non-custodial and compliant payment application, OKX Pay will be embedded within the OKX App, currently available in select markets with a full global rollout expected in the coming months.

2026年3月22日

A New Chapter: Building the Next Generation of Financial Infrastructure Together

The collaboration between OKX and the Intercontinental Exchange (ICE) marks a significant moment for OKX — and carries equally profound meaning for the evolution of the entire digital assets market. ICE builds and operates the world's most critical financial infrastructure, including the New York Stock Exchange and global derivatives and clearing platforms. This strategic investment by ICE in OKX and its addition to our Board of Directors reflects our shared conviction that digital assets technology will transform financial markets.

2026年3月10日

Celebrating Another Year of Building with Determination

As OKX's CEO and a builder who stays true to the original mission, I take great pride in reflecting on the remarkable growth and progress OKX achieved this year. Despite the challenges, 2024 was a year marked by focus, innovation, and resilience. We not only expanded and optimized our products, but also made significant strides in launching transparent and regulation-compliant localized businesses, while further strengthening our global management team. It is worth noting that after going through

2026年1月29日

2025: Steady Progress Toward Financial Freedom

— An End-of-Year Letter to Global Users from Star, Founder and CEO of OKX. "Financial freedom" is often misunderstood. It doesn't mean the absence of rules — rather, it means having the freedom to choose even when rules exist — and more importantly, that the system remains reliable and effective when truly put to the test. This is precisely what we remained focused on throughout 2025. First and foremost, I want to express my sincere gratitude to our global customers, partners, and regulators.

2026年1月16日

OKX Officially Launches in Germany and Poland

By Erald Ghoos, CEO of OKX Europe. Today is a significant day for OKX — and for crypto users across Europe. We have officially launched our fully compliant centralized cryptocurrency trading platform in Germany and Poland! For us, this is more than just a geographic expansion — it is a commitment to building the future of cryptocurrency the right way: secure, transparent, and tailored to local needs. If you are in Germany

2025年10月21日

Partnership Upgrade! OKX and Standard Chartered Join Forces to Expand into Europe

On October 15, Erald Ghoos, CEO of OKX Europe, stated that OKX is expanding its strategic partnership with Standard Chartered to the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE, launching a Collateral Mirroring program — a

2025年10月15日