OKX Research Institute: The Impact of Rising U.S. Treasury Yields on Bitcoin

Abstract

Recently, U.S. Treasury yields have risen at a significantly accelerated pace. In early January, U.S. Treasury yields broke through 1.0%, and on February 25, they surged past 1.5%, rising 50 basis points in less than a month and causing market turbulence. The rise in U.S. Treasury yields is driven by both inflation rates and real interest rates. From a supply-demand perspective, aggressive fiscal policy has led to the Federal Reserve's absorption rate falling short of supply, widening the U.S. Treasury supply-demand gap and pushing yields higher; from a real interest rate perspective, effective pandemic control and vaccine rollouts have improved expectations for economic recovery, significantly restoring consumer confidence. Meanwhile, fiscal stimulus has further boosted consumer demand, coupled with continued constraints on major oil-producing nations, driving oil prices higher and exacerbating inflation.

Theoretically, rising U.S. Treasury yields will lead to a stock market decline. Currently, mainstream models for assessing intrinsic stock value include the Discounted Cash Flow (DCF) model and the Dividend Discount Model (DDM). However, in either model, the primary influencing factors are the risk-free rate rf and the expected market return E(rm). The risk-free rate can be represented by U.S. Treasury yields, which affect the WACC in the denominator of the DCF model and the denominator in the DDM model. Therefore, rising U.S. Treasury yields will lower market expectations. By analogy to high-risk assets, Bitcoin prices will also be affected.

Against the backdrop of continuously rising U.S. Treasury yields, even breaking through the 1.64% high point, the Federal Reserve is unlikely to make an abrupt policy turn. Monetary easing will continue throughout 2021. Even if global central bank easing measures marginally slow, monetary policy exit will be gradual. Investors' long-term inflation expectations are rising, with the overall stock market trending upward, but high-valuation assets are under renewed pressure, particularly leading tech stocks which have suffered severely. Precious metals like gold and silver have also shown weakness over the past five weeks. In an environment of monetary excess and disappointing alternatives like gold, the cryptocurrency market represented by Bitcoin is gradually moving toward the function of "digital gold," showing strong performance and even breaking through the key $60,000 milestone on March 13.

1 Ten-Year U.S. Treasury Yield Rises Under Influence of Real Interest Rates and Inflation

The yield in the Treasury market has become the benchmark interest rate for financial markets, serving as a barometer for investors to judge market trends, and can be understood as the cost of U.S. dollar funds. Typically, when the Federal Reserve raises interest rates, the 10-year U.S. Treasury yield rises; conversely, the 10-year Treasury yield falls. Recently, with the Fed already at near-zero interest rates, the significant rise in Treasury yields suggests a certain "leading" effect, reflecting market expectations regarding the Fed's quantitative easing policy.

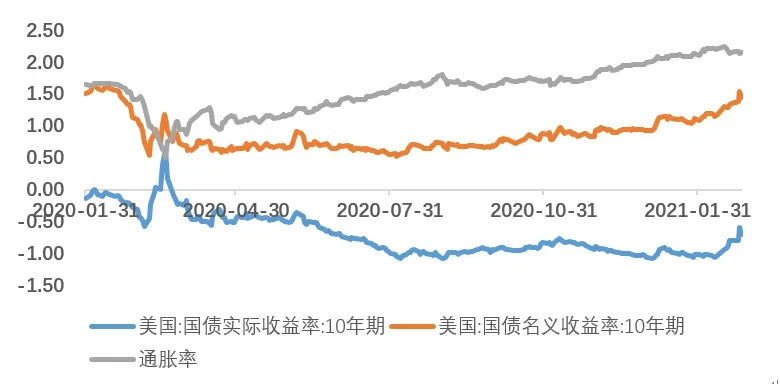

From April to early August 2020, the 10-year U.S. Treasury yield maintained stable low-level operation between 0.5-0.7%. From mid-August to the end of January, Treasury yields began an upward trend. Since the end of January, U.S. inflation rates have maintained a stable trend, so the rise in Treasury yields is primarily caused by real yields. Currently, Treasury yields have exceeded 1.5%, raising concerns in financial markets about inflation.

Figure 1 Rising U.S. nominal, real yields and inflation: January 2020 to present

Source: Wind, OKX Research Institute

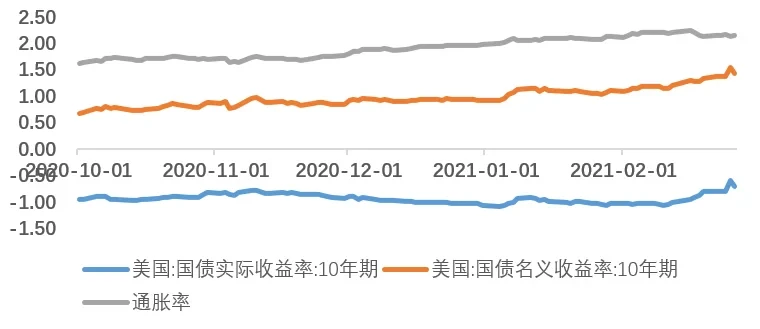

Figure 2 Rising U.S. nominal, real yields and inflation: October 2020 to present

Source: Wind, OKX Research Institute

The Fisher equation indicates that nominal interest rates are influenced by both real interest rates and inflation rates. Therefore, we analyze the reasons for rising nominal rates from two perspectives: U.S. real interest rates and inflation rates.

1.1Improvement in U.S. Pandemic Situation Brings Rising Real Interest Rates

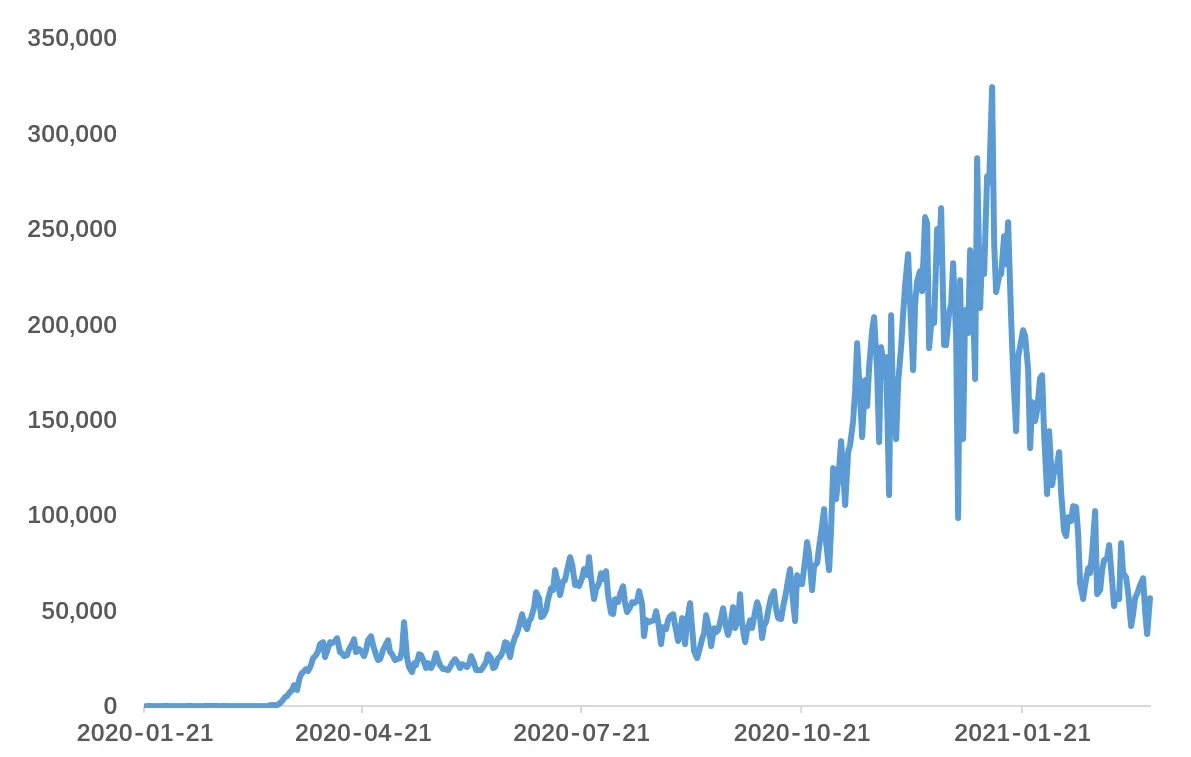

The reason for rising real interest rates is that vaccines have brought improvement to the U.S. pandemic situation. In mid-January, confirmed COVID-19 cases in the U.S. peaked, and since the 15th, confirmed cases have gradually fallen to last October's levels. This is partly the result of the Biden administration's anti-pandemic policies, including mandatory mask-wearing nationwide and implementing stricter lockdown measures. On the other hand, U.S. vaccination has achieved good protective results: since December 14 last year, U.S. vaccination doses have shown an upward trend. Federal data collected by the Centers for Disease Control and Prevention shows that as of March 11, 95.7 million vaccine doses have been administered, with approximately 18.8% of the total population having received at least one dose, and 9.8% having received the full two doses. The U.S. is currently administering over 2.1 million vaccine doses daily.

Figure 3 Decline in New U.S. COVID-19 Cases

Source: Wind, OKX Research Institute

Figure 4 Surge in Daily COVID-19 Vaccinations

Source: Wind, OKX Research Institute

1.2Loose Monetary Policy and Fiscal Stimulus Bring Rising Inflation Rates

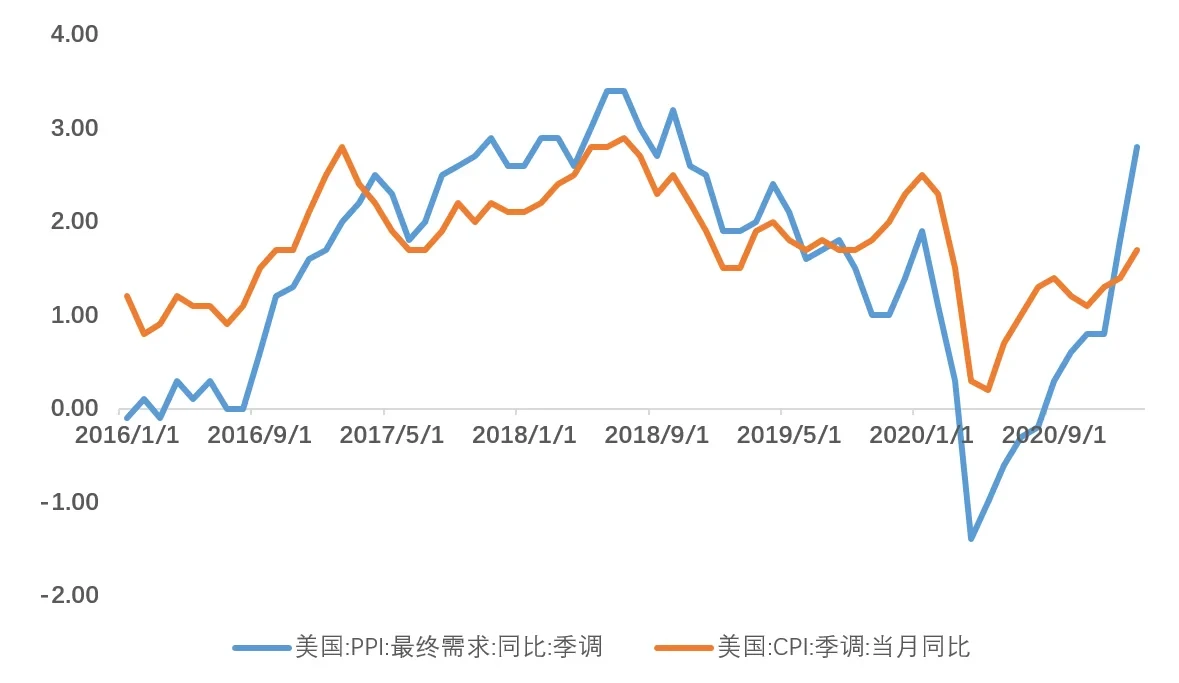

Additionally, rising inflation rates have also pushed up nominal interest rates. CPI can be used to measure the inflation consumers experience in daily living expenses, standing from the consumer's perspective, focusing primarily on price changes in consumer goods, and is a lagging indicator of economic change. PPI, standing from the producer's perspective, measures inflation in the early production process and serves as a leading indicator of economic change. The PCE index incorporates changes in consumer spending habits accompanying price changes, thus better capturing consumer shopping tendencies, and is the inflation expectation measurement indicator preferred by the Fed.

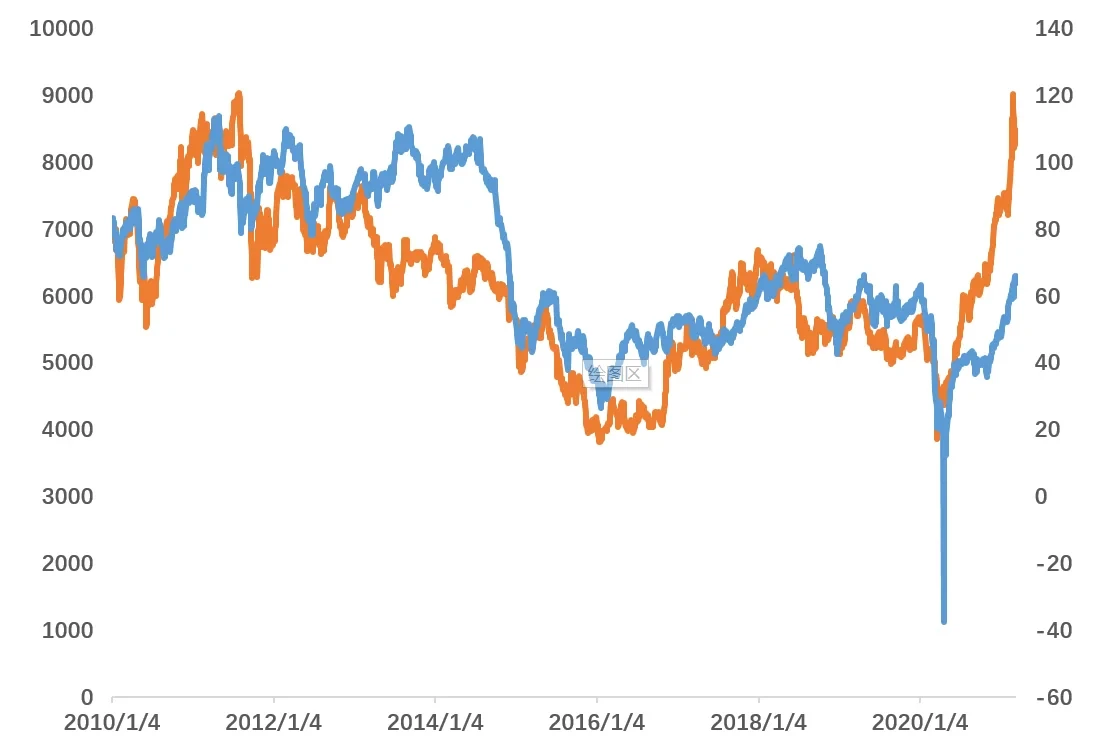

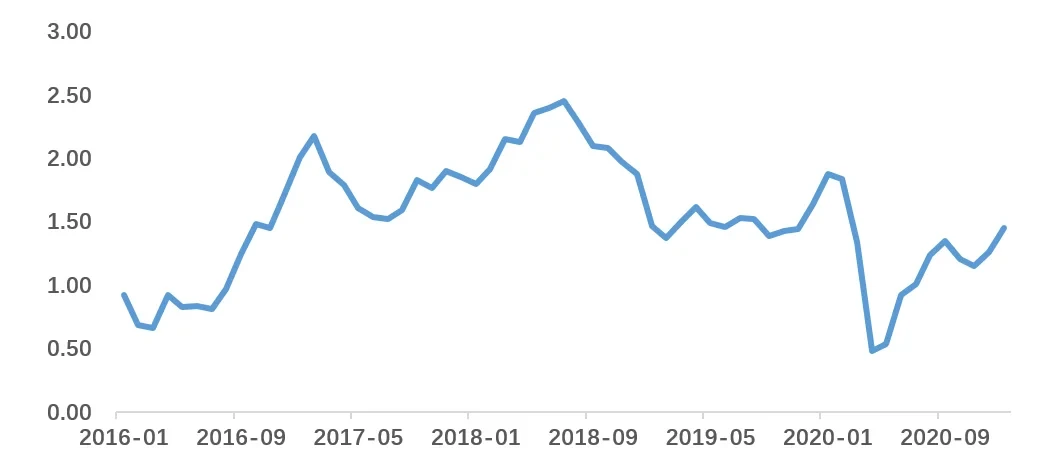

Since the end of 2020, due to supply-demand gaps, global economic recovery, and low interest rates, commodity prices led by crude oil and copper have risen, pushing U.S. PPI growth above expectations, thereby raising interest rates through nominal economic growth channels. Since last October, U.S. WTI crude oil spot prices have risen from $40/barrel to $65/barrel, a growth rate exceeding 60%. As the most upstream energy source, crude oil constitutes cost pressure for all downstream sectors. If oil prices are excessively influenced by supply factors, this will exacerbate U.S. stagflation risks and Fed policy tightening risks, leading to higher U.S. Treasury yields. Copper prices have risen from $6,000 to $8,400 today, an increase of approximately 40%, driving PPI growth above 2.5%. After Q1 2021, with economic marginal slowing, slight recovery in inflation expectations, and structural tightening of credit policy, we are in a transition phase from economic recovery to overheating and stagflation, with a broad liquidity拐 point approaching.

Figure 5 Inflation Recovery at End of 2020

Source: Wind, OKX Research Institute

Figure 6 Rising Copper and Oil Prices at End of 2020

Source: Wind, OKX Research Institute

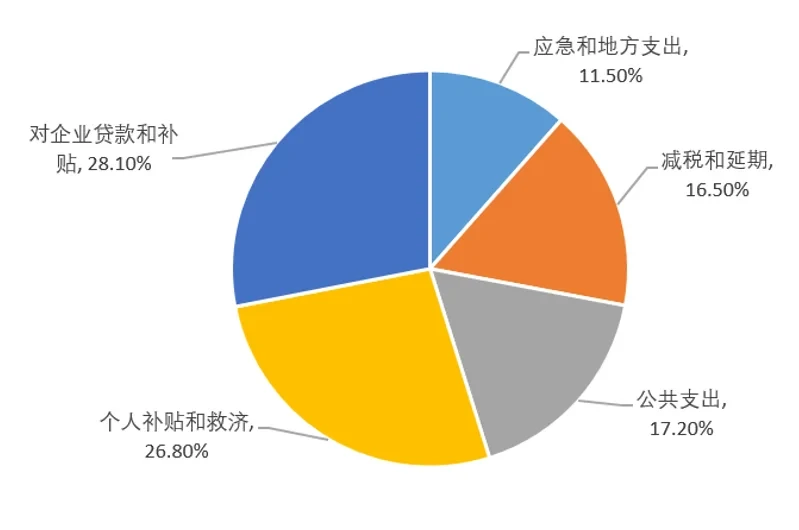

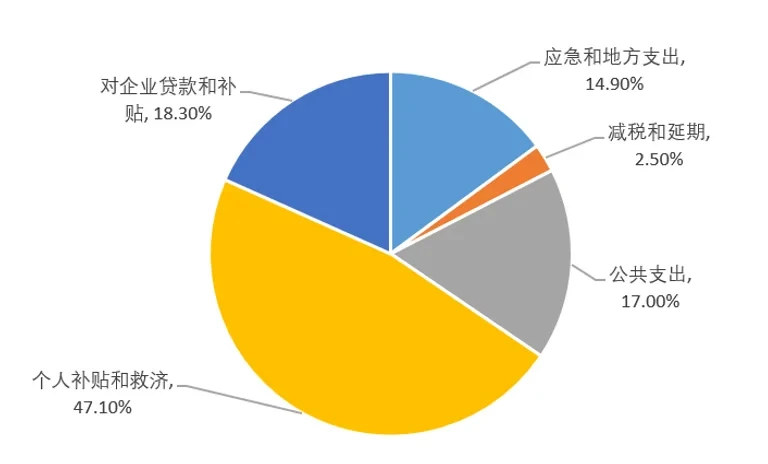

To address the enormous impact of COVID-19 on the U.S. economy, the U.S. government successively passed multiple fiscal stimulus bills in 2020-2021. In 2020, the U.S. passed three rounds of fiscal stimulus, with a total new fiscal deficit exceeding $2 trillion, accounting for 9.7% of 2020 GDP, including the CARES Act passed at the end of March 2020, the PPPHCE passed at the end of April, and the second round of unemployment benefit distribution (LWSPA) passed in early August. In 2021, new U.S. President Biden and Treasury Secretary Yellen passed a "$900 billion stimulus plan" and the "American Rescue Plan Act," totaling a massive $1.9 trillion, exceeding 8.7% of GDP. The proportion of individual subsidies and relief in 2021 (47.1%) far exceeds 2020 levels (26.8%), totaling nearly $900 billion, making it the year with the largest direct subsidies to residents in U.S. history.

Figure 7 2020 Pandemic Government Subsidy Policies

Source: Wind, OKX Research Institute

Figure 8 2021 Pandemic Government Subsidy Policies

Source: Wind, OKX Research Institute

The U.S. $1.9 trillion fiscal stimulus policy is expected to strengthen improved economic expectations and bring larger-scale U.S. Treasury issuance. The upward pressure on Treasury supply will primarily be reflected in rising interest rates. Additionally, excessive fiscal stimulus exacerbates supply-demand imbalances for goods, which will drive up U.S. core goods inflation. From the goods demand perspective, fiscal subsidies will increase income for individuals and companies, thereby driving goods consumption. However, on the goods supply side, excessive unemployment subsidies will crowd out low-wage employment positions, slowing industrial production recovery. Demand for goods clearly exceeding supply will undoubtedly drive up U.S. core goods inflation.

Figure 9 Rising U.S. PCE in 2021

Source: Wind, OKX Research Institute

According to the "Monetary Policy Report" submitted by the Federal Reserve to Congress on February 19, the Federal Open Market Committee will maintain the federal funds rate near zero to achieve maximum employment and 2% inflation over a longer period. The FOMC has maintained the target range for the federal funds rate at 0% to 0.25% since last March, and in the revised amendment published in August reiterated that inflation will remain at 2% in the short term and is expected to moderately exceed 2% for some time. Therefore, the market has dispelled the idea of short-term monetary policy changes.

2 Stock Market and Bitcoin Through the Lens of Rising U.S. Treasury Yields

2.1 Rising Risk-Free Rate Affects Denominator of Pricing Models, Lowering Stock Market Expectations

As the world's most important risk-free rate level, U.S. Treasury yields serve as the "anchor" for risk asset pricing. Because the U.S. government adopted a $1.9 trillion aggressive fiscal policy, leading to fiscal deficits, it is highly likely to issue large amounts of Treasury bonds to increase revenue. From the Fed's perspective, Treasury supply far exceeds demand, undoubtedly causing the surge in Treasury yields.

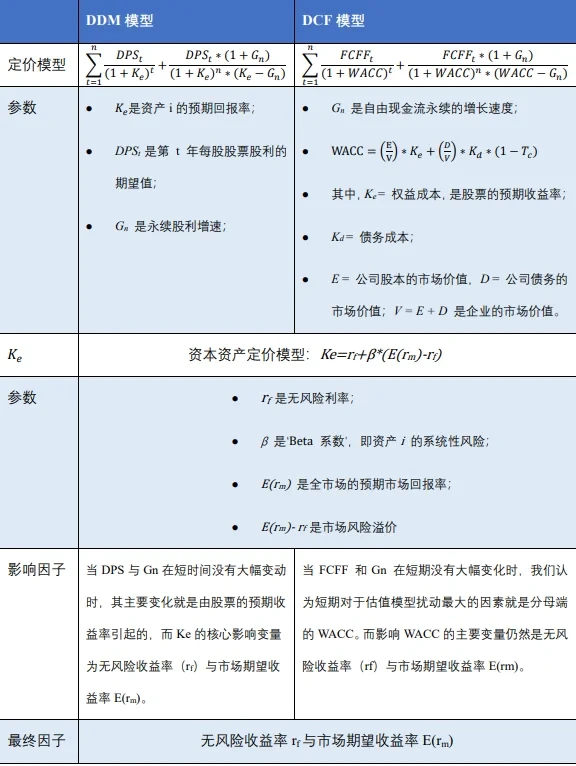

Traditional models for assessing intrinsic stock value include the Discounted Cash Flow (DCF) model and the Dividend Discount Model (DDM). The risk-free rate can be represented by Treasury yields, which affect the WACC in the denominator of the DCF model and the denominator in the DDM model. Therefore, rising Treasury yields will lower market expectations for stocks. By analogy to high-risk assets, Bitcoin prices will also be affected.

Table 1 Mainstream Valuation Pricing Models

Source: Wind, OKX Research Institute

The risk-free rate is commonly represented by Treasury yields, as Treasury bonds are backed by national credit and are typically considered risk-free when the political system is relatively stable. Meanwhile, we typically assume that market risk premium remains stable in the short term, so expected market returns also follow changes in the risk-free rate. All these factors make Treasury yields set the tone for risk asset pricing.

Furthermore, global economic integration is quite mature, with the U.S. ranking first globally in total GDP for nearly 130 consecutive years, accounting for 24.82% of global economic output in 2020. Thus, the status of the U.S. dollar as an international currency is widely accepted, and the Fed's position as a central bank is unparalleled. On the basis of determining Treasury yields as the risk-free rate, U.S. Treasury yields have undisputedly become the "anchor" for global asset pricing.

**2. 2.**Market Expects Fed to Accelerate Current Monetary Policy Shift, Causing Market Panic

On the other hand, Treasury yields are a key indicator for market expectations regarding Fed monetary policy. Since the COVID-19 outbreak in 2020, U.S. unemployment has risen significantly, and financial markets have been weak. To gradually restore the economy, the Fed has continuously increased borrowing, with Treasury yields rising accordingly. Over the past period, Treasury yields have consistently remained at high levels. On March 11, the day after the U.S. Biden government's $1.9 trillion fiscal stimulus bill passed, Treasury yields even broke through 1.64%.

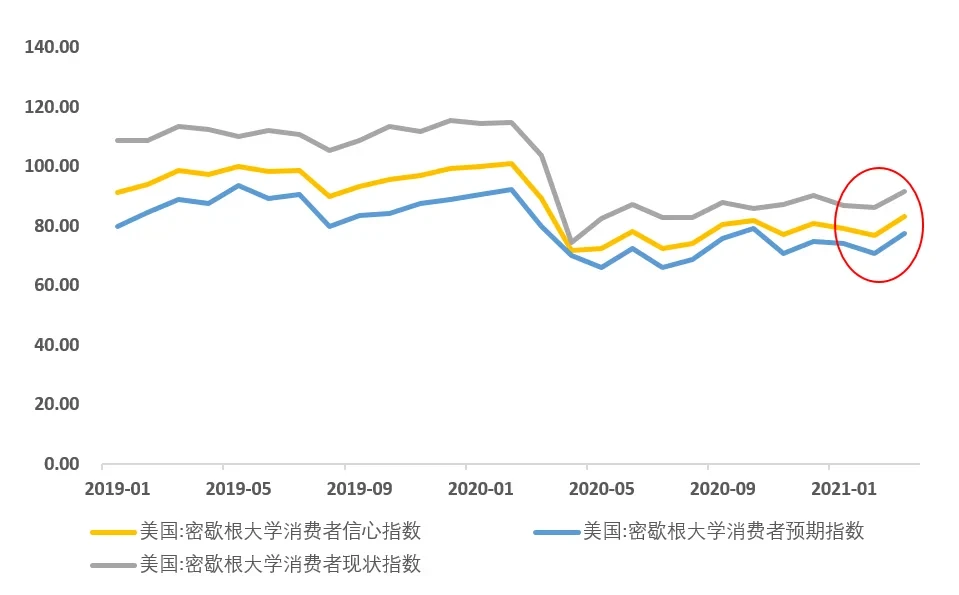

As noted earlier, overseas vaccines have begun to roll out, undoubtedly providing a good foundation for rapid economic recovery. February CPI showed an upward trend, PPI rose even more than expected, unemployment improved moderately, consumer confidence was significantly restored, and fiscal stimulus further boosted consumer demand, coupled with continued constraints on major oil-producing nations and rising oil prices. Currently, barring surprises, steady U.S. economic recovery in 2021 is virtually certain.

Figure 10 Consumer Confidence Showing Upward Trend

Source: Wind, OKX Research Institute

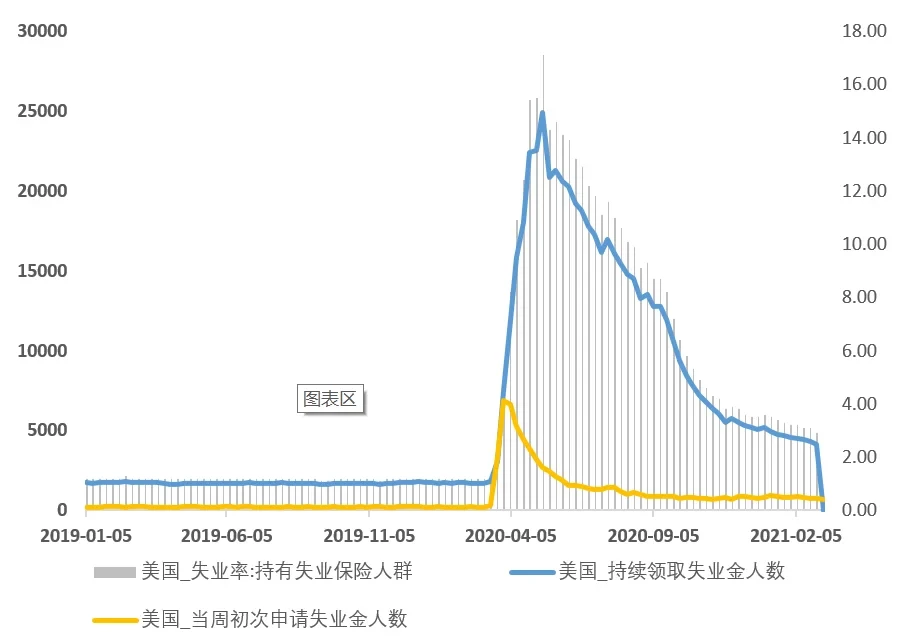

Figure 11 U.S. Unemployment Rate Declines, Unemployment Rate Falls to 2.90% (Unit: thousands, seasonally adjusted)

Source: Wind, OKX Research Institute

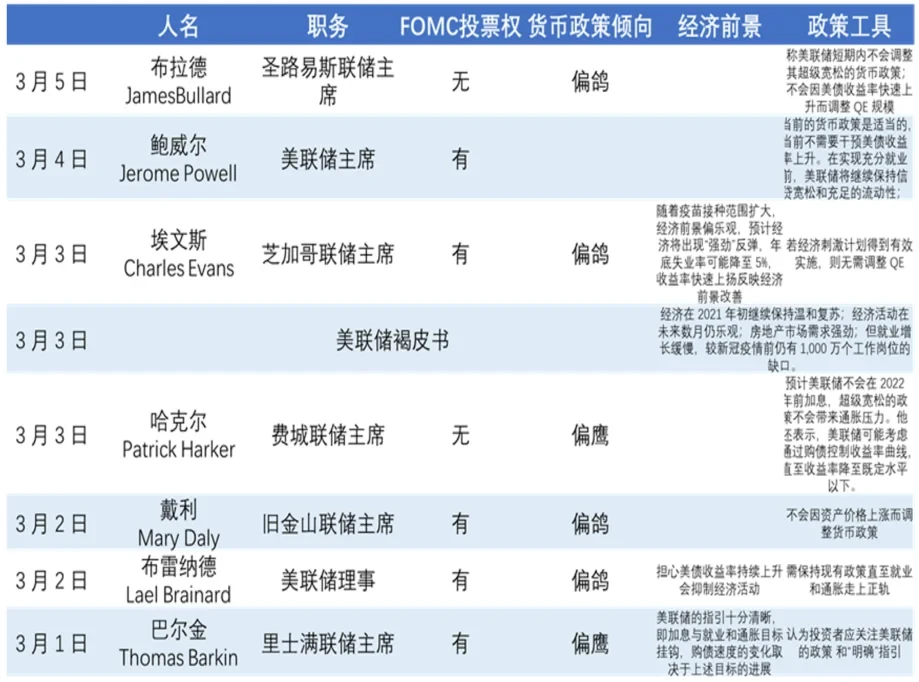

Market sentiment has also been reassured. In recent public statements from Fed officials, almost no one believes inflation will become a threat. Chairman Powell stated that inflation will not rise significantly or sustainably, while also believing that "rising Treasury yields reflect market confidence, indicating a strong economic recovery" and "the economy is still far from achieving substantial progress in employment and inflation." Fed policy is unlikely to make an abrupt turn. Monetary easing will continue in 2021. Even if global central bank easing measures marginally slow, monetary policy exit will be gradual.

Table 2 Summary of Important Views from Fed Officials, March 2021

Source: Wind, OKX Research Institute

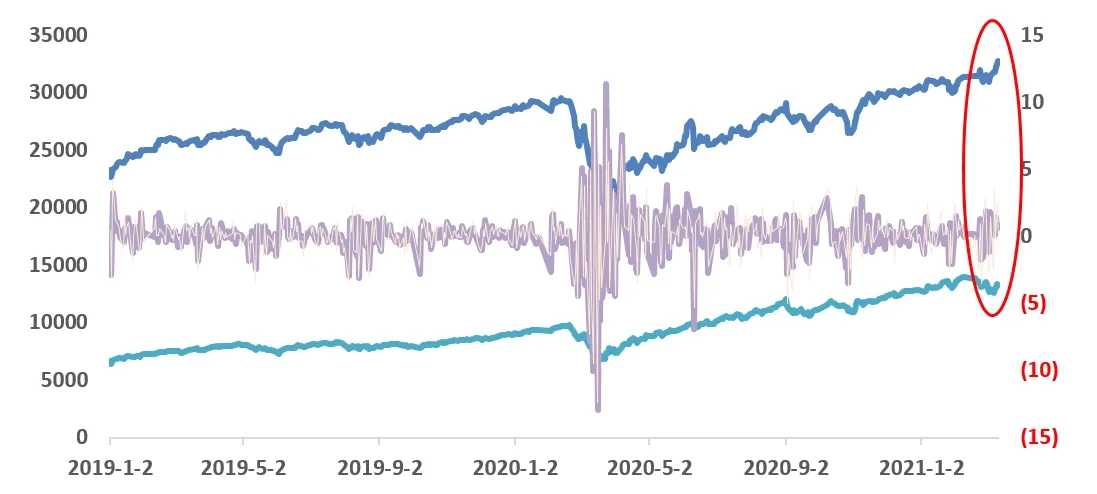

The combination of multiple factors has led to rising Treasury yields "as the times require." Against this backdrop, global financial markets have experienced violent volatility. The overall stock market has trended upward, but high-valuation assets are under renewed pressure, particularly leading tech stocks which have suffered severely. On March 12, the Nasdaq fell 78.81 points, or 0.59%, closing at 13,319.86, while the Dow Jones Industrial Average rose 0.90% to 32,778.64. The relative performance differential between value stocks and growth stocks has returned to pre-pandemic levels.

Figure 12 March 12: Nasdaq Falls 0.59%, Dow Rises 0.90%

Source: Wind, OKX Research Institute

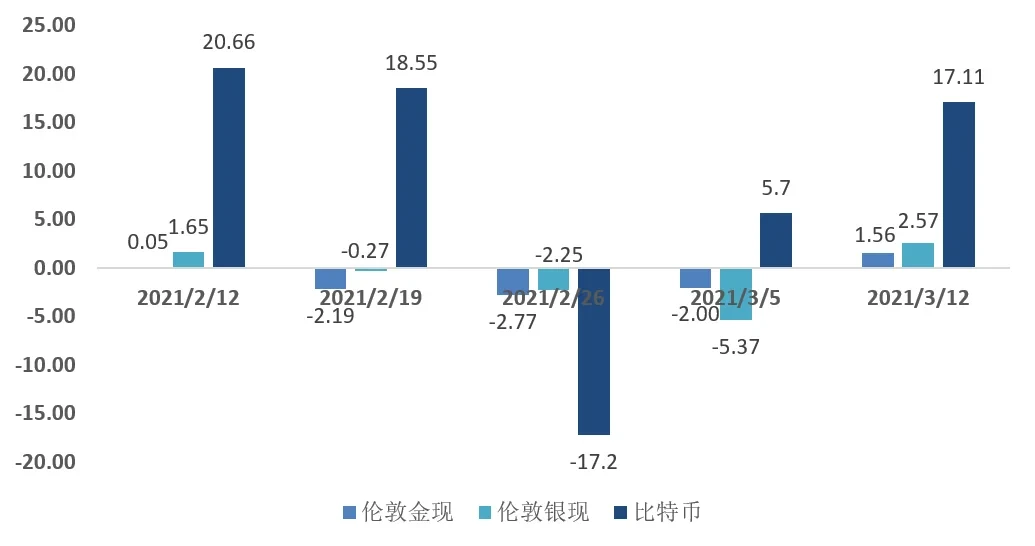

The cryptocurrency market represented by Bitcoin has also shown strong performance, accelerating upward and breaking through the $60,000 milestone on March 13 to reach $61,165.19, a gain of 6.80%. This partly depends on its strengthening monetary attributes, as institutional investors have successively joined, making Bitcoin and other cryptocurrencies move from retail-dominated fringe assets closer to mainstream assets. But to a greater extent, it reflects rising long-term market inflation expectations. Precious metals like gold and silver have shown weakness over the past five weeks, with gains far below Bitcoin. In an environment of monetary excess and disappointing alternatives like gold, the cryptocurrency market represented by Bitcoin is gradually moving toward the function of "digital gold."

Figure 13 Gold and Silver Precious Metals Under Pressure, Bitcoin Gains Significantly

Source: Wind, OKX Research Institute_

3. Current State and Future of the Bitcoin Market

The current Bitcoin bull market is a product of high inflation expectations. On one hand, affected by the pandemic, global economic recovery will slow over the coming year. On the other hand, central banks have launched extremely loose monetary policies, raising inflation expectations in financial markets. In a high inflation environment, to avoid erosion of nominal principal and pursue higher returns, institutional investors have increased demand for Bitcoin. Similarly, when the global economy begins to recover and major central bank monetary policies begin to tighten, changing market inflation expectations, institutional investors will sell Bitcoin, triggering a Bitcoin price crash.

When the rapid rise in 10-year Treasury yields caused U.S. stock market declines, Fed officials quickly moved to reassure market sentiment, issuing statements that the rise in 10-year U.S. Treasury yields is "appropriate" and reflects economic recovery, therefore they will not change monetary policy, dispelling market concerns about monetary policy shifts and correcting market inflation expectations. From a short-term perspective, if Fed officials' above statements successfully reassure market sentiment, then U.S. stocks and Bitcoin prices will see some recovery in the short term. However, if 10-year Treasury yields continue to surge and market confidence and expectations cannot be reversed, then the crash will continue.

The U.S. policy passed a $1.9 trillion fiscal stimulus package. Unprecedented fiscal stimulus measures will drive social demand growth and push up commodity prices, raising global inflation expectations for a period.

Oil prices are an important exogenous shock factor affecting inflation in Europe, America, and other nations. Affected by production restriction policies of major oil-producing nations and gradual global economic recovery, oil prices are gradually rising, which will bring inflation pressure to major European and American economies.

As global electric vehicle giant Tesla, the world's largest asset management company BlackRock, Norwegian oil giant Equinor, and other enterprises successively invest in Bitcoin, Bitcoin is gradually evolving from a niche alternative investment of the past to a "digital gold" for the general public. Benefiting from effective pandemic prevention and control globally, U.S. fiscal policy stimulus, and strong expectations for global economic recovery, in the context of high future inflation expectations, Bitcoin with a fixed total supply cap has become a good asset for fighting inflation, receiving market favor with continuously rising prices. It can be expected that if the economy continues to recover in the second half of this year and loose monetary policy remains unchanged, Bitcoin is highly likely to rise again.

Disclaimer: Digital asset trading involves significant risk. This material should not serve as the basis for investment decisions, nor should it be construed as advice to engage in investment trading. Please ensure you fully understand the risks involved and invest cautiously. OKX Academy provides information only and does not constitute any investment advice. Users' investment actions are unrelated to this site.

Disclaimer

This article may contain product-related content not applicable to your region. This article is intended to provide general information only and does not take responsibility for any factual errors or omissions herein. This article represents only the author's personal views and does not represent OKX's views. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets (including stablecoins) involves high risk, may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets suits you based on your financial situation. For questions about your specific situation, please consult your legal/tax/investment professional. The information appearing in this article (including market data and statistics, if any) is for general reference only. While we have taken all reasonable precautions in preparing these data and charts, we accept no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in full, or excerpts of 100 words or less may be used, provided such use is non-commercial. Any reproduction or distribution of the entire article must prominently state: "Copyright © 2025 OKX. Used with permission." Permitted excerpts must cite the article name and include attribution, for example "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may be generated or assisted by artificial intelligence (AI) tools. Derivative works or other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Opening a New Era of Next-Generation Crypto Payments

The choice of tens of millions of users. Register with OKX to enjoy ultimate trading experience and diverse wealth management products. A letter from OKX CEO Star: Today, we officially launch the first version of OKX Pay to over 100 million global users. As the industry's first payment application to truly achieve non-custodial and compliant integration, OKX Pay will be embedded within the OKX App, currently available to select markets, expected to fully launch within months

March 22, 2026

New Chapter: Building Next-Generation Financial Infrastructure Together

The partnership between OKX and Intercontinental Exchange (ICE) marks an important moment for OKX and holds equally profound significance for the evolution of the entire digital assets market. ICE establishes and operates the world's most important financial infrastructure, including the New York Stock Exchange and global derivatives and clearing platforms. This strategic investment by ICE in OKX and joining our board reflects both parties' shared belief—digital assets technology will transform financial markets

March 10, 2026

Tribute to Another Year of Forging Ahead

As CEO of OKX and a builder who remains true to our original mission, I am proud to look back on OKX's extraordinary growth and progress this year. Despite numerous challenges, 2024 has been a year of focus, innovation, and resilience. We have not only expanded and optimized our products but also made important progress in launching transparent and compliant localized businesses, while further strengthening our global management team. Notably, after experiencing

January 29, 2026

2025: Steady Progress Toward Financial Freedom Together

— Annual Letter from OKX Founder and CEO Star to Global Users "Financial freedom" is often misunderstood. It doesn't mean absence of rules, but rather having the right to choose when rules exist—and when the system is truly tested, it remains reliable and effective. This is exactly what we have focused on throughout 2025. First, I want to extend my sincere gratitude to global customers, partners, and regulatory authorities

January 16, 2026

OKX Officially Launches in Germany and Poland

Author: Erald Ghoos, CEO of OKX Europe Today is significant for OKX—and for crypto users across Europe. We have officially launched our fully compliant centralized cryptocurrency trading platform in Germany and Poland! For us, this is not just geographic expansion, but a commitment to building the cryptocurrency future the right way: secure, transparent, and meeting local needs. If you're in Germany

October 21, 2025

Partnership Upgrade! OKX Partners with Standard Chartered to Expand European Market

On October 15, OKX Europe CEO Erald Ghoos stated that OKX is expanding its strategic partnership with Standard Chartered to the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE to launch the collateral mirroring program—a

October 15, 2025