OKXOKX Research Institute: A Discussion on Several Controversial Issues of Uniswap V3

DAI-0. 01%

Just like Apple's developer conferences, which are hailed as "a feast for tech enthusiasts," Uniswap—a highly anticipated star project in the DeFi space—recently released its new version. Unlike the classic V1 and V2 versions, Uniswap's latest V3 introduces several new features: liquidity aggregation, multi-tier fee tiers, and oracle upgrades, among others.

Based on the actual response to Uniswap V3's release, the reception has been mixed, with widely varying opinions. Some have praised it enthusiastically, while others have expressed disappointment. In light of this, we have carefully selected several noteworthy issues for discussion. It should be emphasized that in many cases, due to differing definitions and standards, conclusions on the same issue may vary. Therefore, let us approach Uniswap V3 from different angles with a mindset of seeking common ground while respecting differences.

1. Is Uniswap V3 an Order Book Model?

Following the release of Uniswap V3, many DeFi community leaders viewed it as a degraded order book model, arguing that Uniswap V3 introduced the "Range Orders" feature, which allows liquidity providers (LP) to deposit digital assets within a custom price range above or below the current price.

However, to dismiss Uniswap V3 as a regression to an order book model based solely on this would be underestimating its innovative nature. In fact, if one carefully examines the design philosophy behind Uniswap V3, it becomes clear that Uniswap V3 is not an order book model at all—Uniswap V3 introduces "price ticks" for AMM, allowing LP to place assets across different price ranges, which in no way alters the operating mechanism of the Automated Market Maker (AMM)!

In traditional order book trading, whether under an auction system or a market maker system, both parties need to place orders (containing price and quantity) onto the order book, and trading is conducted with price as the signal. In an auction system, the matching requirement is to buy and sell assets at the prices most favorable to both parties. Similarly, in a market maker system, market makers must quote buy and sell prices in advance, and investors can only place trading orders after seeing the quotes. From this, we can see that in an order book, liquidity providers actively quote prices, and the market executes trading according to the "price priority" principle, thereby fulfilling the price discovery function.

Figure 1. Schematic Diagram of an Order Book Under an Auction System

In Uniswap V3, however, LP do not actively quote prices at all—they merely place liquidity across different price ranges! The trading price on Uniswap V3, just like Uniswap V2, is still driven by liquidity (adding Asset x or Asset y to the contract) rather than order instructions. The trading price is determined by the ratio of the two assets in the asset pool, meaning it still lacks a price discovery function.

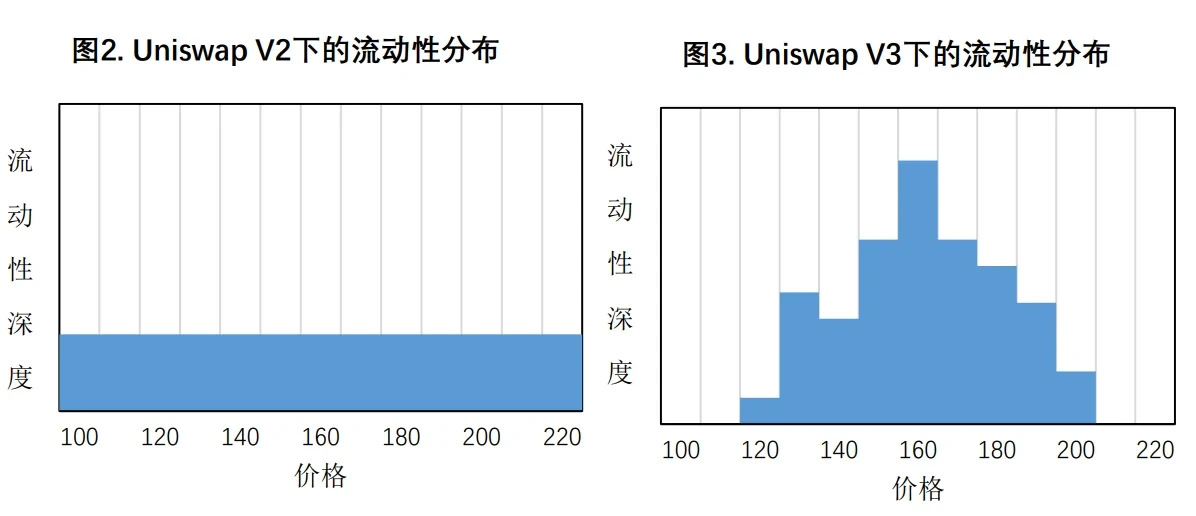

To make an analogy: if the liquidity design in Uniswap V2 is like a water tank where liquidity provided at each price level is the same; then Uniswap V3, in terms of its design principle, is more like a water tank with slotted compartments installed. LP can place liquidity into different price range "slots" based on market prices, as illustrated below.

Therefore, Uniswap V3 has not degenerated into an order book model—it has merely introduced "price ticks." It is a wolf in sheep's clothing. As for the Range Orders feature, the terminology in the Uniswap V3 whitepaper is more precise: "Range Orders" is more akin to a limit order strategy—when the price crosses a given price range, the position held by the liquidity provider transitions entirely from one asset to another.

2. Has Uniswap V3 Really Improved Capital Efficiency?

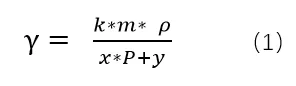

One of Uniswap V3's major features is improving capital efficiency through "liquidity aggregation." In economic terms, capital efficiency can be measured using the following formula:

Capital Utilization = Revenue / Assets

On Uniswap, assets refer to the liquidity LP provides to Uniswap, while revenue comes from trading fees. Trading fees, in turn, are related to the number of trades, the average trade size, and the fee rate. Assuming no changes in asset prices and no LP entry or exit, capital utilization over a given period can be expressed as follows:

Where k is the number of trades over that period, m is the average trade size, ρ is the fee rate, x is the quantity of Asset X in the asset pool, y is the quantity of Asset Y in the asset pool, and P is the price of X relative to Y.

From formula (1), it is clear that to improve capital utilization on an AMM, one must either increase trading volume or fees, or reduce the value of assets in the asset pool.

So, how does Uniswap V3 improve capital utilization? Uniswap's official website provides a case study:

_Both Alice and Bob want to provide liquidity in Uniswap V3's ETH/DAI pool. Each of them has $1 million. To achieve the same liquidity depth, Uniswap V2 requires a deposit of 500,000 DAI and 333.33 ETH (total value of $1 million); whereas in Uniswap V3's $1,500–$1,750 price range, _only 91,751 DAI and 61.17 ETH (total value of approximately $183,500) are needed, thereby improving capital efficiency.

From this, it is clear that the key to Uniswap V3's improved capital utilization lies in reducing the total value of the asset pool (x*P+y).

However, upon reviewing the above example, there always seems to be something amiss. Has Uniswap V3 truly improved capital utilization for AMMs?

A clear example: suppose Uniswap V2 and Uniswap V3 both generate 1,000 DAI in trading fees over a given period. Similarly, all LP on the platform provide liquidity worth 100,000 to both Uniswap V2 and Uniswap V3. Then, according to formula (1), the capital utilization of Uniswap V2 and Uniswap V3 is identical.

From this, it is evident that evaluating Uniswap V3's capital efficiency involves matters of perspective and stance.

From an individual perspective, if someone concentrates all of their liquidity within a specific price range, their personal capital utilization can improve; however, the overall market capital efficiency has not necessarily improved as a result.

Additionally, Uniswap V3's capital efficiency optimization design only considers the individual, ignoring the impact of other market participants on oneself—this is known as an externality in economics.

What is an externality? Using the example from Uniswap V3's official website: the designers believed that in V3, if a person has $1 million in liquidity, they only need to deposit 91,751 DAI and 61.17 ETH (total value of approximately $183,500). But in reality, when there is $1 million in liquidity on the market, and if people believe the future price will only fluctuate within the $1,500–$1,750 price range, then from the perspective of rational decision-making, every LP would place their liquidity within that range. As a result, Uniswap V3 would still have a total of $1 million in liquidity deposited. In this case, there is essentially no difference between Uniswap V2 and Uniswap V3—capital efficiency remains the same.

**More importantly, Uniswap V3 raises fairness concerns. ** In Uniswap V2, all LP have equal standing, and the trading fees they earn are distributed equally. However, Uniswap V3 aggregates liquidity through the "Range Order" mechanism to improve capital efficiency. At the same time, Uniswap V3 stipulates that when the market price falls within the set price range, LP can earn trading fees; whereas when the market price moves outside the price range, that portion of liquidity will no longer earn fees.

This inadvertently introduces a liquidity competition mechanism into Uniswap V3—organized, professional LP will adjust the price range of their liquidity in real time based on market price movements to maximize their returns; whereas ordinary LP find it difficult to make timely adjustments, resulting in lower capital efficiency and fee shares.

Therefore, on the whole, the "liquidity aggregation"—which Uniswap V3 values most highly—has not fundamentally improved the platform's overall capital utilization. Instead, the liquidity competition it triggers will give rise to fairness issues and increased Gas costs from LP repositioning. This is a net loss.

Disclaimer: Digital asset trading involves significant risk. This material should not be relied upon as an investment decision-making basis, nor should it be interpreted as advice on investment trading. Please ensure you have a thorough understanding of the risks involved and invest cautiously. The OKXOKX Academy provides information for reference only and does not constitute any investment advice. All investment activities by users are unrelated to this site.

Disclaimer

This article may contain information about products not available in your region. This article is intended solely to provide general information and makes no representation as to any factual errors or omissions. This article represents the author's personal views and does not represent the views of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holdings in digital assets (including stablecoins) involve a high degree of risk and may fluctuate significantly or even become worthless. You should carefully consider whether trading or holding digital assets is appropriate for you based on your financial situation. For questions specific to your circumstances, please consult your legal/tax/investment professional. The information contained in this article (including market data and statistics, where applicable) is provided for general reference purposes only. While all reasonable precautions have been taken in preparing such data and charts, we accept no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, or excerpts of 100 words or fewer may be used, provided that such use is non-commercial in nature. Any reproduction or distribution of the full article must prominently state: "This article is copyrighted © 2025 OKX, used with permission." Permitted excerpts must cite the article name and include attribution, for example, "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may have been generated or assisted by artificial intelligence (AI) tools. Derivative works and other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Ushering in a New Era of Next-Generation Cryptocurrency Payments

The choice of tens of millions of users. Register with OKX to enjoy an exceptional trading experience and a diverse range of wealth management products. A letter from OKX CEO Star: Today, we are officially launching the first version of OKX Pay to over 100 million global users. As the industry's first truly non-custodial and compliant payment application, OKX Pay will be embedded directly within the OKX App, and is currently available in select markets with a full global rollout expected in the coming months.

March 22, 2026

A New Chapter: Building the Next Generation of Financial Infrastructure Together

The partnership between OKX and the Intercontinental Exchange (ICE) represents a significant milestone for OKX and holds equally profound implications for the evolution of the entire digital assets market. ICE builds and operates the world's most critical financial infrastructure, including the New York Stock Exchange and global derivatives and clearing platforms. This investment by ICE Select in OKX and its joining of our board of directors reflects our shared conviction—that digital assets technology will transform financial markets.

March 10, 2026

Reflecting on Another Year of Building with Determination

As the CEO of OKX and a builder who stays true to his original vision, I take great pride in looking back on the extraordinary growth and progress OKX has achieved this year. Despite formidable challenges, 2024 was a year marked by focus, innovation, and resilience. We not only expanded and optimized our products, but also made significant strides in launching transparent and regulation-compliant localized businesses, while further strengthening our global management team. It is worth noting that after going through

January 29, 2026

2025: Steady Progress Toward Financial Freedom

— A Year-End Letter to Global Users from Star, Founder and CEO of OKX "Financial freedom" is often misunderstood. It does not mean the absence of rules, but rather having the freedom to choose—even in the presence of rules—and having a system that remains reliable and effective when truly put to the test. This is precisely what we focused on throughout 2025. First and foremost, I would like to express my sincere gratitude to our global customers, partners, and regulators.

January 16, 2026

OKX Officially Launches in Germany and Poland

By Erald Ghoos, CEO of OKX Europe Today marks a significant moment for OKX—and for cryptocurrency users across Europe as a whole. We have officially launched our fully compliant centralized cryptocurrency trading platform in Germany and Poland! For us, this is more than just a geographic expansion—it is a commitment to building the future of cryptocurrency the right way: safe, transparent, and tailored to local needs. If you are in Germany

October 21, 2025

Partnership Upgrade! OKX Joins Forces with Standard Chartered to Expand into Europe

On October 15th, Erald Ghoos, CEO of OKX Europe, stated that OKX is expanding its strategic partnership with Standard Chartered into the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE to launch the collateral mirroring program—a

October 15, 2025