DeFi Data Rebounds Again: A First Look at Lending Protocol Interest Rate Models

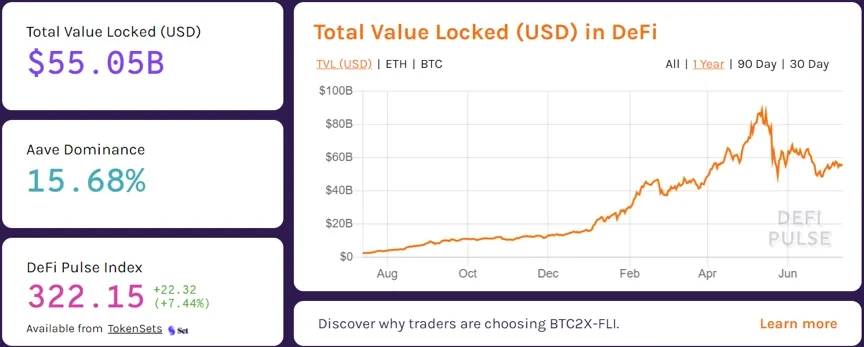

After seven years of deep accumulation and one year of explosive growth, DeFi has finally achieved the remarkable results we see today. According to third-party data site DeFiPulse, the total value locked (TVL) in Ethereum-based DeFi has reached $55.05 billion, representing a 21.4x growth within one year. Of this $55.05 billion in TVL, lending protocols account for nearly half, reaching $28.99 billion.

Ethereum-based DeFi total value locked, source: DeFiPulse

DeFi lending protocol total value locked, source: DeFiPulse

From this data comparison, lending protocols can be considered a well-deserved cornerstone of DeFi. Of course, beyond the total value locked in lending protocols, their security, ease of use, and convenience are even more noteworthy. Generally speaking, DeFi lending protocols are a relatively mature emerging method of generating stable returns using crypto assets. After years of operational practice, although some asset loss events caused by smart contract vulnerabilities have occurred, objectively speaking, no systemic incidents threatening the underlying foundation of DeFi lending protocols have ever occurred. Moreover, the protocols have continued to develop healthily despite multiple severe market turbulence events. These basic facts demonstrate that lending protocols now possess strong attack resistance, and their security has stood the test of time. Additionally, DeFi lending protocols allow anyone to lend their held crypto assets to earn returns without undergoing KYC, and achieve trustlessness in asset deposit, custody, and redemption through transparent smart contracts, greatly lowering the barrier to participation in financial activities.

More importantly, borrowing users can leverage DeFi lending protocols to convert their different types of crypto assets into unified tokens provided by smart contracts, shuttling the same assets and reusing them across different DeFi protocols, thereby multiplying the efficiency of capital utilization in the crypto space. They can also flexibly combine with other DeFi protocols to achieve automated operation of multi-layered, multi-level, complex, and nested financial trading. Whether in DEXs or aggregators, lending protocols are frequently seen. In this colorful and flexible financial "Lego" game, DeFi lending protocols should not be underestimated.

Having understood the important position of DeFi lending protocols in the current DeFi ecosystem, the following will focus on the interest rates of DeFi lending protocols as an entry point, further discussing mainstream DeFi lending protocols and their interest rate models.

What Are the Mainstream DeFi Lending Protocols?

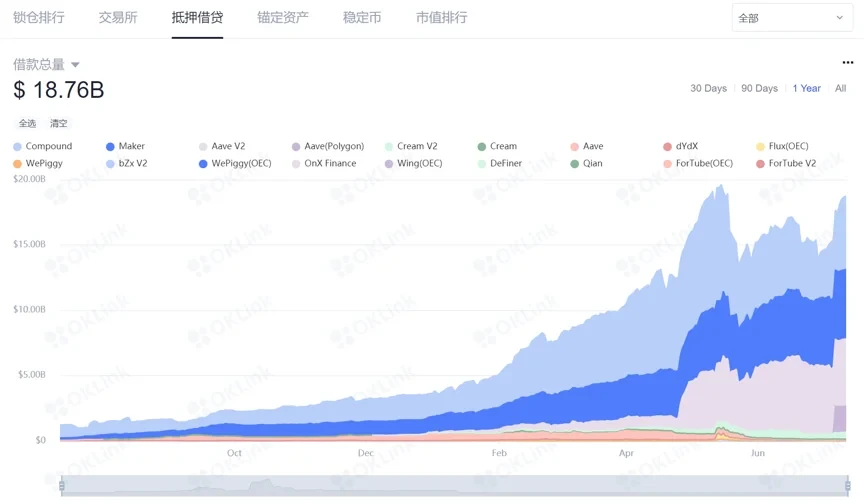

If we refer to the ChainMaster section under OK Link, which ranks collateral protocols by total borrowing volume, the top three are Compound, Maker, and Aave V2.

DeFi lending protocol borrowing volume overview, source: OKLink — ChainMaster

Regarding Compound, we mentioned it when introducing the one-year anniversary of "DeFi Summer." Compound started in 2018, and currently has a total borrowing volume of $5.63 billion and a total deposit volume of $12.74 billion. Last June, Compound protocol was the first to release its governance token COMP, thereby popularizing the concept of Staking, and COMP further led the market's liquidity mining boom. As an open-source protocol based on the Ethereum blockchain, it allows users to borrow against or lend collateral. More importantly, Compound allows its users to access compound liquidity pools anytime, anywhere, and also allows users to deposit different types of crypto assets such as ETH and BAT to earn returns.

Regarding Maker, ranked second, it is actually the earliest-developed project among DeFi lending protocols. MakerDAO was already launched in 2014. Currently, MakerDAO has a total borrowing volume of $5.31 billion and a total deposit volume of $11.91 billion. Maker (MKR) is the native governance token of the MakerDAO protocol, primarily providing support for DAI stablecoin functionality and price stability, reducing price volatility of the DAI stablecoin. In the MakerDAO protocol, users are provided with a simple option to create a Collateralized Debt Position (CDP) on its smart contracts, through which they can lock ETH and other crypto assets to generate DAI. In terms of Payment, users can use MKR and DAI for trading. Once the CDP is closed after the trading is approved, MKR tokens and DAI are completely burned, thereby maintaining the security of user assets on smart contracts and the stable operation of the lending protocol.

Aave V2 ranks third, but the gap with the top two is not significant. Currently, Aave V2 has a total borrowing volume of $5.14 billion and a total deposit volume of $12.37 billion. It can be said that in terms of both borrowing and deposit volumes, all three are essentially at the same level. Aave V2 is the upgraded version of AAVE. The original AAVE project was called ETHLend, launched in September 2017, and upgraded to V2 in December 2020. According to the ChainMaster section under OK Link, Aave V2 added return and collateral swap functions, flash liquidation functions, gas optimization solutions, and fixed and floating borrowing rate functions. Among these, the fixed and floating borrowing rate function upgrade has attracted the most market attention.

DeFi Lending Protocol Interest Rate Models

In this section, we will use Compound, which ranks first in borrowing volume as discussed above, as an example to briefly understand the interest rate models in DeFi lending protocols.

Compound lending protocol is essentially a crypto assets pool that dynamically calculates changes in supply and demand between borrowers and lenders based on the fund needs of different investors in the crypto market, through established smart contracts, and provides floating interest rates. Lenders (Suppliers) and borrowers in the crypto market can directly interact with the protocol to earn interest at floating rates or pay interest.

This process easily draws parallels with banks in the traditional financial world. In fact, Compound lending protocol does indeed play the role of a bank in the crypto market. First, let's look at how we apply for a mortgage through a bank in the traditional financial world.

Taking common residential mortgages as an example, in the US, banks generally set the maximum mortgage rate at no more than 75%. That is, when a borrower uses a house worth $1 million as collateral to apply for a mortgage from a bank, the bank will lend at a ratio not exceeding 75% of the collateral's market value. If this loan is approved, the borrower can receive a maximum of $750,000. As long as the borrower makes regular loan and interest payments to the bank, they can keep the house. If the borrower defaults on payments, the bank will sell the house to recover the loan and interest, with any excess returned to the borrower.

For banks, the money comes from depositors, and large amounts of deposits converge to form a fund pool that can be used for any form of lending. Depositors receive interest from the bank for their deposits. A bank is a fund pool, and depositors are not bound to any specific borrower, which means depositors can withdraw their funds from the bank at any time and demand the bank to pay interest for the deposit period at the agreed rate.

What Compound does is bring the traditional banking model onto Ethereum smart contracts, and solve the problems of fund pools and interest rates. Simply put, it uses the Ethereum underlying ledger system and employs smart contracts to maintain a real-time settlement ledger. When a trading occurs, the ledger performs a settlement of accounts, at which point the settlement interest is updated to the account balance. When the next trading event occurs, it triggers another such settlement process and updates the balance. This completes a real-time, complete, auditable asset liability statement and cash ledger, i.e., cash + borrowing = deposits + collateral assets.

To illustrate, in the Compound protocol, we create a new DAI lending market, which generates a new smart contract. The smart contract records all the information of this newly created DAI lending market. When the DAI lending market opens, users A, B, and C (lenders) deposit into the USDC fund pool as follows:

A deposits 2000 DAI, B deposits 3000 DAI, and C deposits 5000 DAI. At this point, the DAI fund pool has 10,000 DAI. Assuming we do not consider floating borrowing rates or profits, and only ensure balanced accounts where borrowing revenue = deposit interest, the following two conclusions are respectively valid: 1) Borrowing revenue = total borrowing volume * borrowing rate * time

2) Deposit interest = total deposit volume * deposit rate * time.

From this, we can further derive the following conclusion: 3) Total borrowing volume * borrowing rate = total deposit volume * deposit rate

From conclusion 3, we can deduce: a) if total borrowing volume is 0 (nobody borrows), no revenue is generated and the deposit rate is 0; b) as total borrowing volume increases and revenue grows, the deposit rate also increases; c) if total borrowing volume remains unchanged (revenue unchanged), but total deposit volume increases, the deposit rate decreases. Finally, we can conclude: interest rates change as total borrowing and deposit volumes change.

Now, if we set the overcollateralization rate of the DAI fund pool at 25%, then user D (borrower) can borrow a maximum of 75% of the fund pool. Assuming D borrows 2500 DAI at a 5% borrowing rate and repays the principal of 2500 DAI plus 125 DAI in interest, the DAI fund pool's return rate is 1.25%.

That is, (2500*5%)/10000, return rate = (total borrowing volume * borrowing rate) / total deposit volume

At the same time, we can derive the fund utilization formula: 25% = 2500 / (7500 + 2500), Fund Utilization UR = borrowing / (cash + borrowing)

Further simplifying the deposit rate formula: 1.25% = 5% * 25%, deposit rate = borrowing rate * fund utilization

In a short-term lending market, if the borrowing rate is too low, no one is willing to lend money because the return is too low. On the other hand, if the borrowing rate is too high, no one is willing to borrow because the borrowing cost is too high, and the net return on borrowed money is too low. Therefore, how to maintain a reasonable and healthy borrowing rate has always been the direction that various DeFi lending protocols continuously strive for. It is precisely for this reason that during AAVE's upgrade to V2, the fixed and floating borrowing rate functions attracted格外 market investors' attention.

Conclusion

Finally, let's bring our focus back to the secondary market. Since the market bottomed out at the end of last month, DeFi lending protocol concept tokens represented by COMP have all achieved不错的涨幅. According to OKX market data, COMP has risen from $197 on June 22 to above $430, an increase of over 118%.

Recent COMP price trend, source: OKX

Not just COMP, but also AAVE, MKR, and leading projects in other DeFi sectors such as UNI in the DEX space, have all performed well in the secondary market recently. Moreover, from multiple data dimensions such as Compound's total value locked, deposit volume, and borrowing volume over the past two weeks, there are signs of recovery. Hopefully, after experiencing nearly three months of sluggish market conditions, the crypto market can bring us better news this hot July.

Finally, while we collectively look forward to good news, OKX has also launched the "Contract Summer Campaign, Trade to Win 30,000 USDT" activity. Open the OKX app and click the banner at the bottom of the homepage to participate.

Disclaimer

This article may contain product-related content not applicable to your region. This article is only dedicated to providing general information and is not responsible for any factual errors or omissions. This article represents only the author's personal views and does not constitute the views of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holdings in digital assets (including stablecoins) involve high risk and may fluctuate significantly or even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions about your specific circumstances, please consult your legal/tax/investment professionals. The information in this article (including market data and statistical information, if any) is provided for general reference purposes only. Although we have taken all reasonable precautions in preparing this data and these charts, we do not assume any responsibility for factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety or used in excerpts of 100 words or less, provided that such use is non-commercial. Any reproduction or distribution of the full article must prominently state: "This article is copyrighted © 2025 OKX, used with permission." Permitted excerpts must cite the article name and include attribution, for example, "Article name, [author name (if applicable)], © 2025 OKX." Some content may have been generated or assisted by artificial intelligence (AI) tools. Derivative works and other uses of this article are not permitted.

Show More

Recommended Reading

2025 KOL Most Used OKX Products Checklist

In the cryptocurrency industry, professional players' choices are always direct and pure. In 2025, KOLs cast the most authentic votes for industry tools and ecosystem development with their year-round capital investment and time dedication. We focused on four core questions: "What was your biggest achievement this year?", "Given that achievement, what OKX products do you use most and love in 2025?", "Why do you like it?", "This product

January 5, 2026

2026 Investment Outlook: Assets On-Chain, Intelligence & Privacy | OKX Year in Review

Three major trends for crypto's future: asset transformation, subject transformation, and rule transformation. As we are about to enter 2026, after bidding farewell to four years of focusing on "building roads" for infrastructure, the crypto industry is welcoming a profound paradigm shift. OKX Ventures defines this as the dawn of the "Kinetic Finance" era, where the core is no longer how fast the network is, but the flow of on-chain assets and earning

December 31, 2025

Vote with Data, Insights into 2025 Popular Trading Products | OKX Year in Review

Looking only at market conditions, it's hard to explain the return differences among trading users in 2025. What truly determines returns also depends on account-level operation methods, not just market volatility itself. OKX's annual report shows that mainstream coins remain the core of capital turnover and return carrying, supporting trading and strategy execution; emerging coins are more used to amplify volatility and provide phased opportunities, but are not a stable, long-term source of returns. What truly continuously contributes to returns is

December 30, 2025

Fusaka in Practice: What Ethereum's Latest Upgrade Means for L2, Nodes, and Users

Ethereum mainnet has already completed the Fusaka fork. At the protocol level, this upgrade primarily covers four areas, full text按 Q&A Show More Three guests' core viewpoints and front-line experience: Ahmad (@smartprogrammer) – Nethermind Execution Client / Ethereum Core Dev Manu (@manunalepa) – Prysm / Of

December 16, 2025

OKX Research | Why Did RWA Become a Key Narrative in 2025?

RWA (Real World Assets) is becoming the "new favorite" of global capital. Simply put, RWA is the process of bringing valuable, ownership-bearing things from the real world—such as houses, bonds, stocks, and other traditional financial assets, and even art, private lending, and carbon credits that are usually difficult to trade directly—onto the blockchain, transforming them into tradeable, programmable crypto assets. This means that, on the one hand,

November 20, 2025

Claude Takes the Crown, Truth Behind 6 Major AI Grid Strategies | OKX & Ai Coin Live Test

The short-term trading champion , is it also the king of grid strategies? NOF1's "AI Trading Live Arena" first season finally concluded on November 4, 2025, at 6 AM, whetting the appetites of the crypto, tech, and finance circles. However, the outcome of this "AI IQ public test" was somewhat unexpected—the six models' combined $60,000 in principal was only $4.3

November 6, 2025